.avif)

Perovskite solar cells have emerged as one of the most promising photovoltaic technologies of the 21st century. These thin-film photovoltaic cells utilize a perovskite structured compound, typically a hybrid organic-inorganic lead or tin halide-based material, as the light-harvesting active layer. Crucially, they're able to absorb light across nearly all visible wavelengths, and thanks to recent advances in their manufacturing, they've achieved a meteoric rise from 3.8% efficiency in 2009 to certified efficiencies for single junction solar cells exceeding 26% today: a development trajectory unprecedented in the history of solar cell research.

Named after the ABX3 crystal structure they share with the mineral perovskite (CaTiO₃), these materials combine exceptional optoelectronic properties with potentially low-cost solution processing, offering a pathway to extremely cheap solar energy. While single crystalline silicon solar cells require energy-intensive processing at temperatures exceeding 1400°C with complex purification steps to achieve 99.9999% purity, perovskite solar cells can be fabricated through simple solution processing methods like spin-coating or printing at temperatures below 150°C, potentially reducing manufacturing costs by orders of magnitude.

The technology's appeal extends beyond simple efficiency metrics: perovskites enable flexible, lightweight, and semi-transparent solar cells suitable for building integration, indoor energy harvesting, and space applications where traditional silicon photovoltaic cells face limitations.

However, the journey from scientific novelty to commercial reality presents formidable challenges. Stability under real-world conditions, lead toxicity concerns, and scalable manufacturing remain critical barriers. The field stands at a pivotal juncture where fundamental scientific breakthroughs must translate into industrial solutions, requiring unprecedented coordination between academia, industry, and policymakers.

To better understand where the field of perovskite solar cells is headed, we conducted a comprehensive analysis of the CAS Content Collection™, the largest human-curated repository of scientific information. After examining substances, concepts, sections, and bibliometric information, we identified key trends shaping the technology's future: the emergence of lead-free alternatives, revolutionary interface engineering approaches, and the critical gap between academic discovery and industrial implementation. These analyses provide essential insights for researchers identifying collaboration opportunities, industry professionals evaluating investment strategies, and policymakers crafting frameworks for a sustainable energy transition.

The evolution of perovskite solar cell research

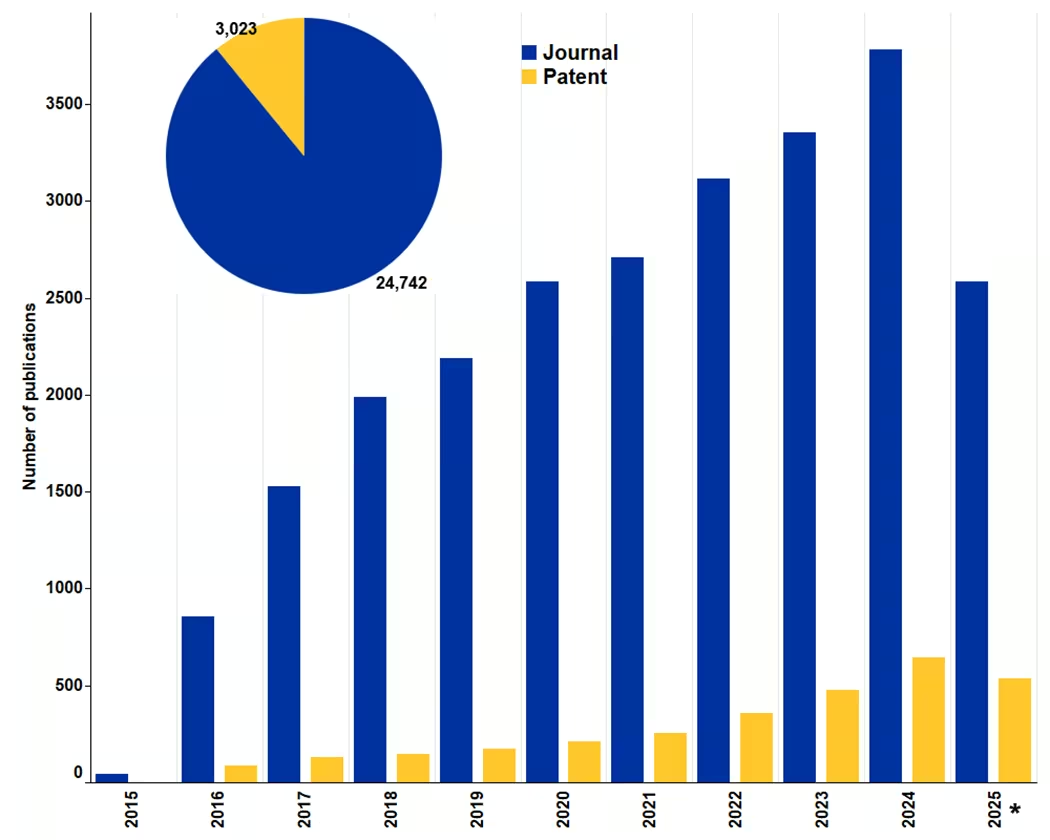

The perovskite solar cell field has experienced remarkable growth since 2015, with journal publications increasing 86-fold from 44 in 2015 to 3,782 articles by 2024, demonstrating sustained academic momentum (see Figure 1). Patent activity, while starting later, also shows accelerating commercial interest with a surge from single patent in 2015 to 645 in 2024.

The percentage of patents has steadily risen from 2% (2015) to 15% (2024). This trajectory reflects a maturing technology where fundamental discoveries are increasingly translated into proprietary innovations, though significant research-to-commercialization gaps persist.

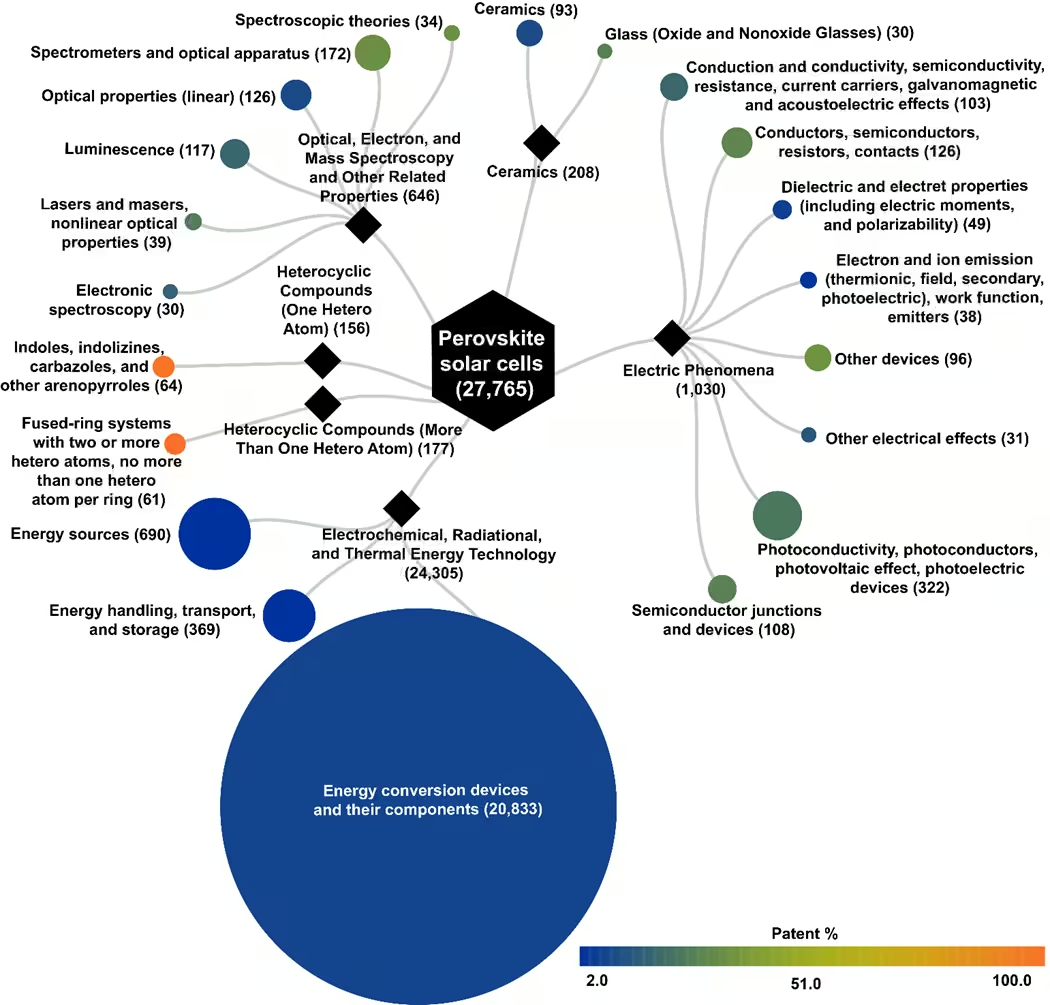

Publications in the CAS database are classified into CAS sections according to their reported processes or substances. These sections represent broad scientific research areas and are further organized into subsections for more granular research categorization. This sectional framework enabled us to analyze and visualize the research landscape across the publication dataset (see Figure 2).

This analysis revealed a field dominated by energy technology research, with 24,305 publications in Electrochemical, Radiational, and Thermal Energy Technology representing the core research domain. Within this section, energy conversion devices and components account for 86% of publications, though with a modest 7.5% patent ratio, indicating that while device development dominates academic research, much of this work remains pre-commercial or focuses on fundamental understanding rather than proprietary innovations.

In the Electric Phenomena section, patent activity varies dramatically across subsections. "Other devices" shows high commercialization at 34.4% of patents, while semiconductor-related subsections maintain robust patent ratios of 23-29%, suggesting strong industrial interest in novel electronic architectures and junction engineering. This contrasts sharply with fundamental studies like electron emission (2.6% of patents), highlighting the commercial emphasis on device-level innovations over basic physics research.

The Optical and Spectroscopy section reveals contrasting subsections: while spectroscopic theories and spectrometer apparatus show high patent ratios (32%), fundamental optical properties research shows minimal commercialization (9.5%). This suggests that innovation in characterization tools and methodologies represents a significant commercial opportunity, even as basic optical studies remain academically focused.

Particularly noteworthy is the extraordinary patent dominance in heterocyclic compounds sections, with near-complete patent representation (98-100%). This indicates that novel organic materials, particularly carbazoles and fused-ring systems used in charge transport layers, represent the frontier of proprietary development, where chemical innovation directly translates to competitive advantage in device performance and stability.

Substances in perovskite solar panel research: Commercial viability and research trends

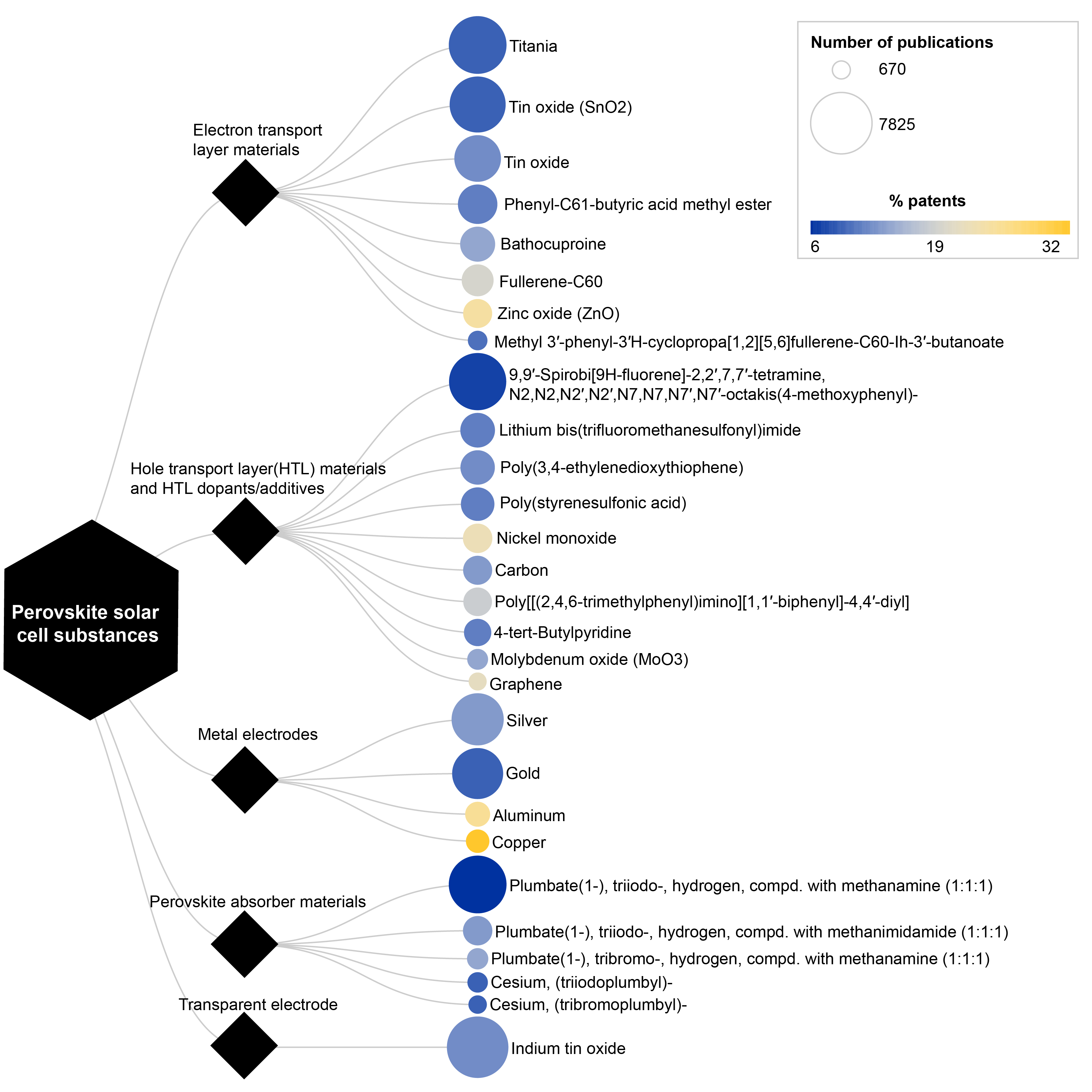

Before we explore research concepts in more detail, let's examine the substances present in the highest number of perovskite solar panel publications. We analyzed the chemical substances reported in these publications using the CAS Registry®, a comprehensive database containing over 279 million registered substances from research literature. What we found revealed distinct patterns in research focus and commercial development trajectories (see Figure 3).

Among electron transport layer (ETL) materials, traditional metal oxides dominate the research landscape, with titania (TiO₂) and tin oxide (SnO₂) appearing in nearly 13,400 publications combined, though showing relatively low patent ratios (9-12%). Notably, zinc oxide demonstrates higher commercial interest with 24% patent representation, suggesting advantages in scalability or processing despite fewer total publications.

The hole transport layer (HTL) materials present a compelling narrative of innovation versus establishment. While Spiro-OMeTAD dominates with over 6,000 publications, its mere 7% patent ratio indicates commercialization challenges, likely related to cost and stability. Conversely, emerging materials like nickel oxide (22% of patents) and graphene (21% of patents) show stronger commercial potential despite lower publication volumes, signaling industry focus toward scalable alternatives.

Metal electrode selection reflects clear cost-performance trade-offs. Gold remains the research standard but shows limited commercial adoption (9% of patents), likely because of this material's high costs. Conversely, copper and aluminum demonstrate the highest patent ratios (32% and 25% respectively), indicating strong industry preference for cost-effective alternatives despite lower research visibility.

The perovskite absorber landscape is dominated by methylammonium lead iodide (MAPbI₃) with nearly 7,000 publications, yet its low patent ratio (6%) highlights stability concerns hampering commercialization. Mixed-cation formulations and bromide-based variants show higher patent percentages (13-14%), suggesting these modifications offer improved commercial viability through enhanced stability and/or performance, critical factors for industrial adoption. The combination of different cations enhances thermal and phase stability and allows for optimal bandgap tuning, resulting in higher power conversion efficiency and operational longevity compared to single-cation counterparts. Bromide and chloride-based perovskites offer wider bandgaps suitable for tandem applications.

The material innovation landscape in perovskite solar cells is shifting toward interface engineering and alternative transport layers, as seen in Figure 4, which visualizes the substances with the highest average year-over-year growth between 2020 and 2024.

![Scatterplot comparing publication counts and average year‑over‑year growth for perovskite solar cell materials. Points show chemicals and oxides, with color indicating patent share. Several phosphonic acids show high growth; P-[2-(9H-Carbazol-9-yl)ethyl] phosphonic acid and nickel oxide have the most publications.](https://cdn.prod.website-files.com/650867962272bf8f15c1034b/698b5a030caefedc07f2e236_image4.avif)

Phosphonic acid-based self-assembled monolayers (SAMs) and carbazole-functionalized variants show high growth: P-[4-(3,6-dimethyl-9H-carbazol-9-yl)butyl]phosphonic acid surged 491% annually, while P-[2-(9H-Carbazol-9-yl)ethyl] phosphonic acid and its dimethoxy derivative grew at 319% and 197% respectively. Remarkably, these materials show zero patent activity despite appearing in 519 combined publications, suggesting this transformative interface technology remains in open scientific development.

The charge transport layer evolution shows divergent commercialization strategies. Copper oxide emerges as a promising hole transport material with 124% growth and 25% patent protection, while nickel oxide (60% growth, 8% of patents) remains primarily academic. Gallium indium zinc oxide (87% growth, 20% of patents) signals growing interest in transparent conducting oxides beyond traditional indium tin oxide (ITO). Iron's surprising presence (92% growth, 60% of patents) likely indicates novel electrode or catalytic applications with strong commercial interest.

Emerging additives reveal sophisticated crystallization control strategies. Methanamine, N-methyl-, hydriodide shows remarkable 233% growth, suggesting novel A-site cation engineering for enhanced stability. The presence of magnesium fluoride (77% growth) and tungsten disulfide (66% growth) indicates exploration of protective layers and 2D material interfaces.

This material evolution demonstrates a clear trend: while breakthrough interface technologies remain in pre-competitive research phases, alternative transport layers and processing additives attract increasing commercial attention, suggesting these represent nearer-term commercialization pathways for industry stakeholders.

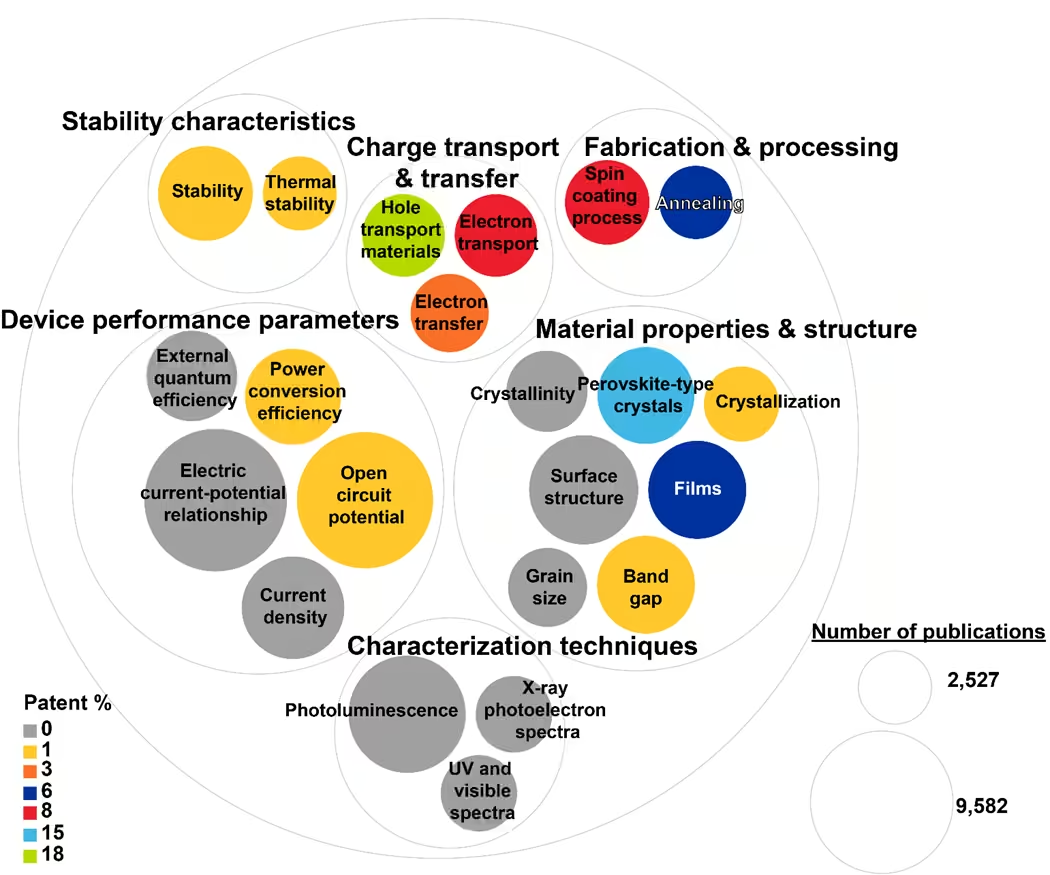

Top CAS concepts in perovskite solar panel publications

We examined CAS-indexed concepts that appeared most frequently in the publications to provide additional insights into perovskite solar cell research trends. The distribution of patents versus journal publications across research concepts reveals a striking contrast between fundamental research and commercial development (see Figure 5).

Characterization techniques, including photoluminescence, UV-visible spectroscopy, and X-ray photoelectron spectroscopy, collectively represent over 12,000 publications yet show zero patent activity. This pattern underscores their role as analytical tools and the foundational infrastructure for scientific understanding, rather than as innovations for commercial differentiation.

Device performance parameters exhibit similarly minimal patent activity (0-1%), despite representing the largest publication cluster with over 31,000 studies. The extensive presence of electric current-potential relationships, open circuit voltage, and power-conversion efficiency in academic literature reflects the field's emphasis on achieving record efficiencies and understanding fundamental science.

A notable shift emerges in the charge transport and fabrication domains. Hole transport materials demonstrate the highest patent ratio at 18%, signaling intense commercial competition in developing proprietary material formulations. Similarly, fabrication processes like spin coating (8% of patents) and annealing (6% of patents) show moderate commercialization, indicating that process optimization represents a key competitive advantage for industrial players.

The material properties category reveals strategic commercial interests, with perovskite-type crystals showing 15% patent activity among 4,427 publications, suggesting significant intellectual property development around novel compositions. Stability, arguably the field's most critical challenge, shows surprisingly low patent activity (1%), potentially indicating that breakthrough solutions remain elusive or that companies are protecting stability innovations through trade secrets rather than patents.

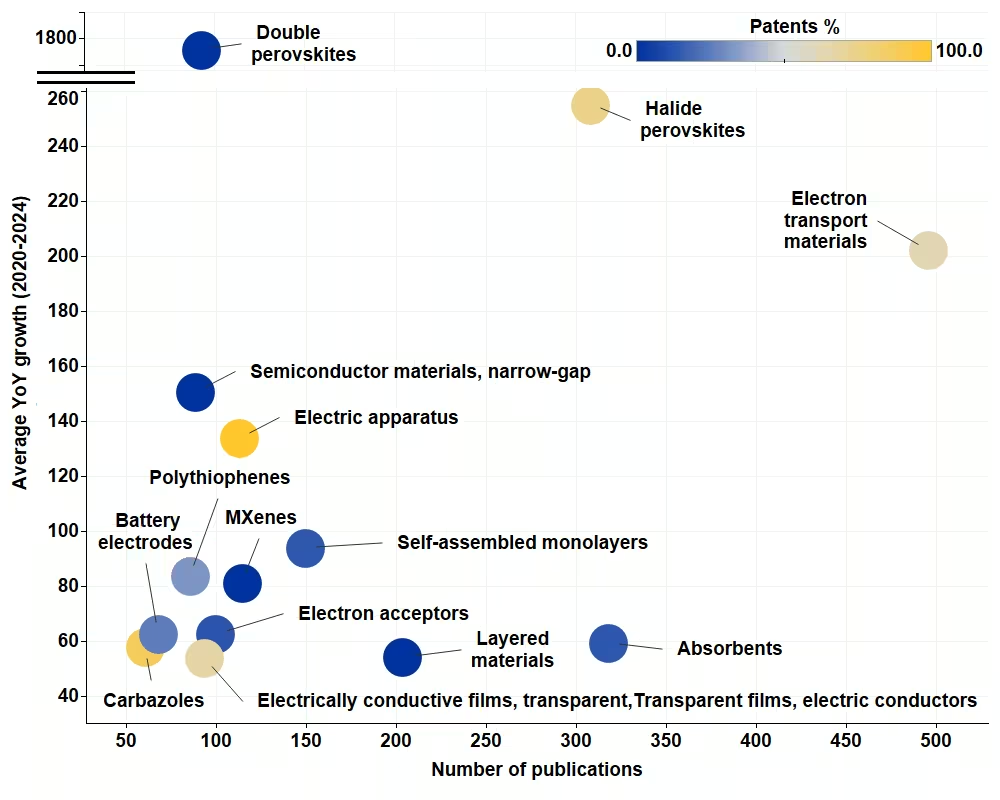

Emerging frontiers in perovskite solar panel research

Turning to the fastest-growing concepts between 2020 and 2024, we see transformative shifts in fundamental science and commercial development (see Figure 6). Double perovskites demonstrate high expansion with 1,778% average year-over-year growth, signaling a paradigm shift toward lead-free alternatives despite zero patent activity (which indicates this remains in exploratory phases). Halide perovskites show remarkable 255% annual growth with 75% patent ratio, suggesting rapid commercialization of compositional innovations.

Materials engineering dominates emerging trends, with electron transport materials experiencing 202% growth alongside 63% patent activity. The surge in self-assembled monolayers (94% growth) and MXenes (81% growth) highlights the field's pivot toward novel two-dimensional materials and precision interface engineering, though low patent ratios indicate early-stage development. The emergence of narrow-gap semiconductors (150% growth) and polythiophenes (83% growth) indicates exploration of alternative architectures for tandem applications and flexible devices.

The gulf between high-growth academic concepts (double perovskites, MXenes) with minimal patents versus moderate-growth commercial technologies (carbazoles at 58% growth, 88% patents) reveals a two-track innovation ecosystem. Academic institutions push boundaries with revolutionary materials, while industry consolidates around incremental improvements to proven technologies. This pattern suggests optimal collaboration opportunities exist where high-growth academic discoveries meet commercial expertise in scaling and stability.

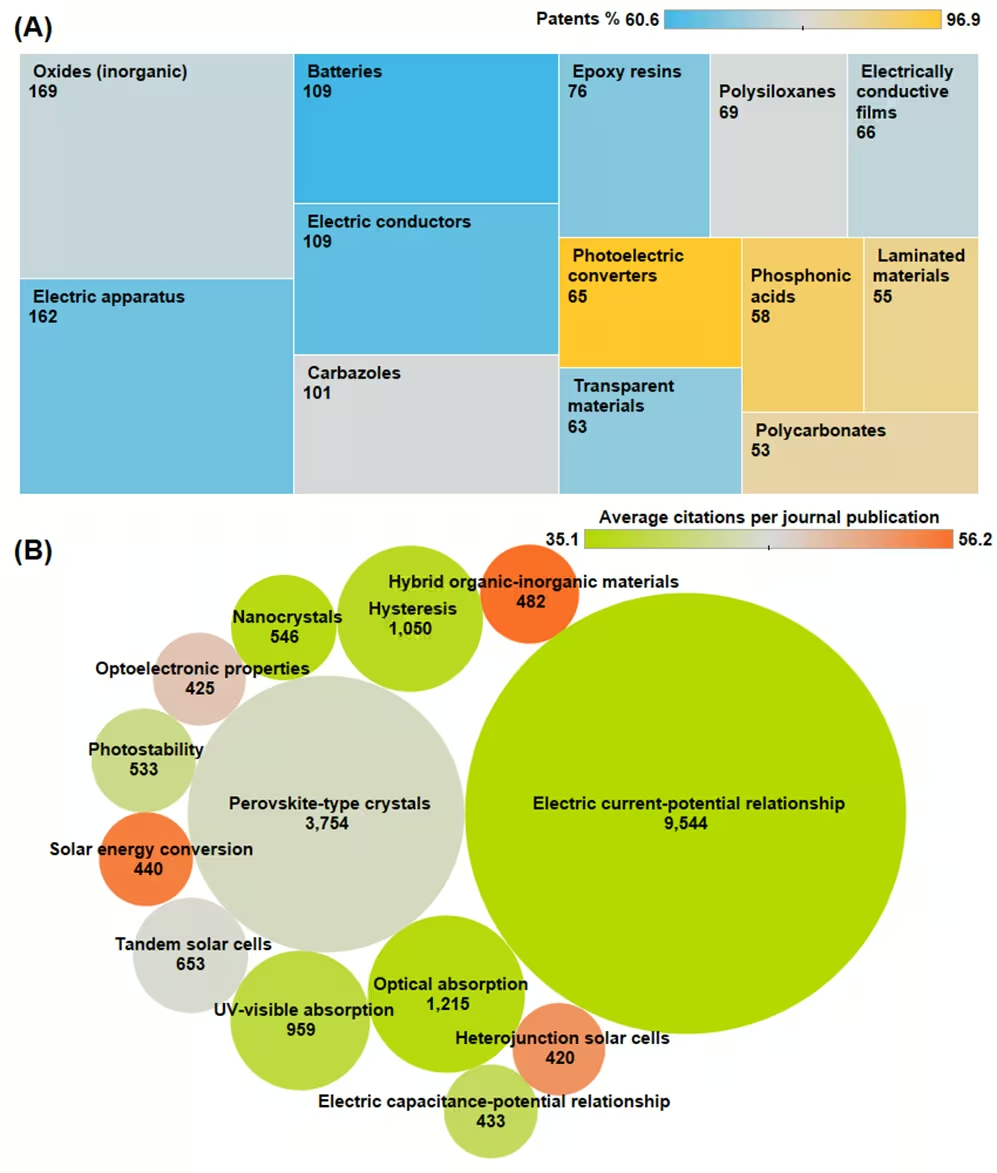

Commercial innovation hotspots in perovskite solar panel technology

As of 2025, the commercialization of perovskite solar cells was limited to tandem cells combined with silicon solar cells. Tandem architectures combining perovskites with silicon have achieved record efficiencies, with Longi Green Energy Technology setting the current world record at 34.6% in 2024 and numerous other manufacturers advancing toward commercial deployment.

We further focused our analysis on patent-intensive concepts to better understand the current strategic commercial focus areas within perovskite solar cell development (see Figure 7A). Photoelectric converters demonstrate near-complete patent dominance (96.9%), indicating this application space is entirely commercially driven. Interface engineering to optimize charge extraction attracts high commercial interest, with phosphonic acids showing 91.4% patent representation, suggesting proprietary self-assembled monolayer technologies.

Encapsulation and stability solutions also dominate commercial innovation, evidenced by high patent ratios in laminated materials (87.3%), polycarbonates (84.9%), and polysiloxanes (78.3%). This concentration reflects industry's paramount focus on solving degradation challenges through proprietary barrier technologies.

The prominence of carbazoles (78% of patents) highlights the intense competition in hole transport material development, while electrically conductive films (76%) and transparent materials (70%) indicate commercial emphasis on electrode optimization.

Notably, the integration potential with energy storage systems is evident from batteries appearing with a 60.6% patent ratio, suggesting industry envisions hybrid perovskite-battery systems. This patent landscape reveals that while academic research explores fundamental physics, commercial entities concentrate on practical implementation challenges that determine market viability like encapsulation, interfaces, and system integration.

Conversely, citation analyses reveal the fundamental research which drives breakthrough discoveries in perovskite photovoltaics. Figure 7B presents the concepts with high average numbers of citations per journal publications and the number of journal publications in which they appeared. Hybrid organic-inorganic materials command the highest average citations, underscoring their revolutionary impact on the field's trajectory. Solar energy conversion and heterojunction solar cells represent transformative architectural innovations that have redefined efficiency boundaries.

The prominence of optoelectronic properties and tandem solar cells in high-impact research indicates that band gap engineering and multi-junction architectures constitute the field's cutting edge. Notably, perovskite-type crystals, despite appearing in thousands of publications, maintain remarkably high average citations, demonstrating sustained scientific interest in compositional innovations.

Critical challenges dominate impactful research, with photostability and hysteresis representing fundamental obstacles requiring breakthrough solutions. The high citation rates for electric current-potential relationships highlight the importance of understanding charge dynamics.

This citation landscape suggests that transformative advances emerge from addressing fundamental material properties, novel architectures, and stability challenges, areas where interdisciplinary collaboration between materials scientists, device physicists, and chemists proves most fruitful.

Future directions for perovskite solar cells in green energy

The perovskite solar cell field stands at a critical inflection point, transitioning from academic phenomenon to commercial reality. Our analysis of over 27,000 publications reveals a technology maturing rapidly yet facing persistent challenges that will determine its impact on green energy. The 86-fold increase in publications since 2015, coupled with accelerating patent activity reaching 15% of publications by 2024, signals growing industrial confidence.

Our data analysis shows three transformative trends which will likely define the next phase of development. First, the explosive growth in lead-free double perovskites and self-assembled monolayer interfaces suggests breakthrough solutions to toxicity and stability challenges may emerge in the coming years. Second, the convergence with energy storage systems, i.e., battery-related concepts showing 60% patent ratios, indicates perovskites may enable integrated photovoltaic storage solutions. Third, the bifurcation between academic exploration of revolutionary materials and industrial focus on incremental improvements creates optimal conditions for strategic partnerships.

Perovskite-silicon tandem cells have achieved 34.6% efficiency with multiple companies approaching commercialization. These could dominate future photovoltaic markets by cost-effectively surpassing single-junction theoretical efficiency limits. Lead-free perovskites based on tin, bismuth, or antimony show promise, with tin-based devices reaching approximately 16% efficiency, though breakthrough innovations in stability and performance remain essential for commercial viability.

For researchers, opportunities lie in addressing the stability-efficiency-scalability trilemma through interdisciplinary collaboration. Industry professionals may need to focus on interface engineering and encapsulation technologies showing the highest patent intensity. Success requires coordinated efforts across the innovation ecosystem, transforming perovskite solar panels from laboratory performance into gigawatt-scale renewable energy solutions essential for achieving global climate goals.